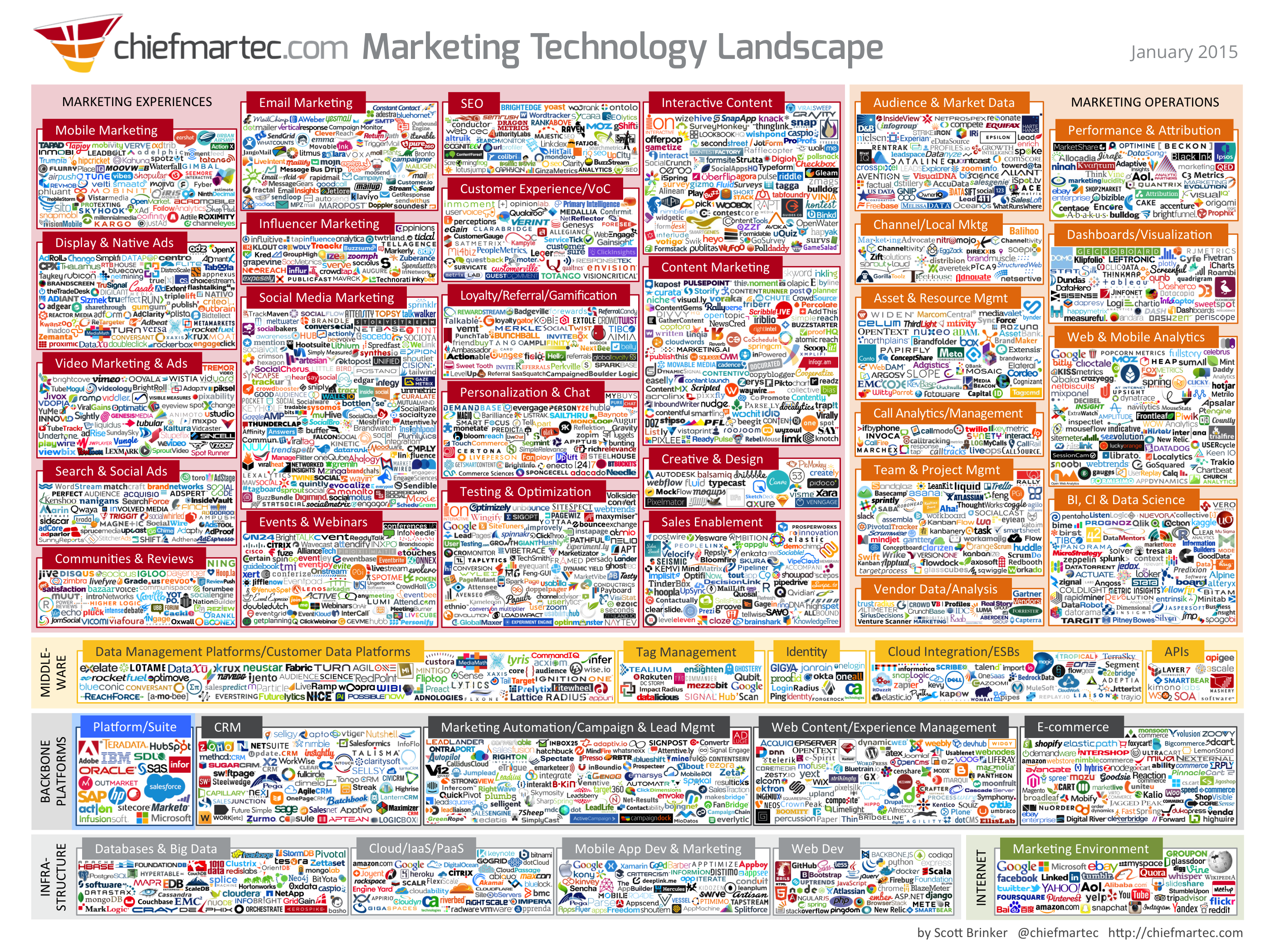

For the past two years, Chiefmartec.com, run by Scott Brinker, has published one of the most mesmerizing and frequently-cited infographics in tech: a definitive map of the Marketing Technology landscape.

This “supergraphic” is so dense that most people treat it like a Monet painting, interpreting the creator’s message from a few steps away. That message: the industry is huge. In fact, the World Marketing Software Forecast predicts that the marketing software industry will exceed $32 billion by 2018 while still growing at over 12% per year, making it “one of the fastest-growing areas in high tech.”

From infographic to data set

This graphic was so compelling that I just had to see the brushstrokes. So I zoomed in — a lot. It quickly became clear that these 1,876 companies were just the starting point. By studying them all just a bit more closely, someone could uncover new insights about the marketing technology industry on an unprecedented scale.

I rolled up my sleeves, fired up Mechanical Turk, and went to work compiling data about these companies, one by one. My first area of focus, and the subject of today’s post, is pricing.

Pricing a technology product is extremely difficult and can sometimes be the difference between a huge success and a total flame-out. I dispatched Mechanical Turk to the websites of all 1,876 companies to discover which companies offered public pricing and just how those products were priced by industry.

Pricing insights

The results of the study are detailed in the sections that follow, and reveal new insights like these:

- More than half of all marketing technology companies do not reveal their pricing publicly

- Only about 16% of companies offer a free tier as part of their offering

- Companies offering a free tier have significantly lower non-free starting prices as well, coming in at less than half the cost of their non-freemium peers.

- Monthly pricing dominates the landscape, with fewer than 20% of companies advertising annual or one-time pricing.

Read on for the full results, and remember to check out RJMetrics if you’re trying to get a handle on your own company’s data.

Is it common for marketing technology vendors to list pricing publicly?

Maybe not as common as you’d think. Even after we omitted companies that weren’t actually paid services, we found that only 40% of marketing technology companies list their pricing publicly. And it’s even less common in certain categories:

Anecdotally, I found that companies justify their lack of public pricing based on solution complexity—there are too many factors, they say, that go into a price. These solutions instead offer demos or other “contact us” forms.

Is freemium a common model for marketing technology companies?

If you want to get more people to convert, you remove friction from the buying process. One way to remove friction is to show pricing publicly. An even better, though perhaps more controversial tactic, is using the freemium model. Of the companies listing their pricing publicly, how many are offering a 100% free tier? The answer? 41% of companies that list pricing publicly have a freemium model, or 16% of all marketing technology companies. Here’s how this breaks down by category:

Here we see that 57% of Middleware companies offer free options, while only 27% of Backbone Platforms are giving users a free pass. This makes intuitive sense, Backbone Platforms are primarily marketing automation and CRM platforms. These types of software can be challenging to implement and require lots of customization, it’s not surprising that freemium is rarely an option.

Here’s how the numbers look as a percentage of all marketing technology companies:

Does freemium impact pricing strategy of paid tiers?

I was curious how this freemium strategy played out in the rest of a company’s pricing strategy. My guess was that freemium offerings would have a low introductory tier that wouldn’t give free users price tag shock if they were considering upgrading to paid customers. Turns out, this is true:

Companies with a free tier start their lowest tier at around $100/month, less than half that for their non-freemium counterparts. This affirms our earlier hypothesis: companies want to have a low-price offering to move freemium customers into a paid tier.

Does a company’s category affect its pricing?

There’s so much variation in MarTech pricing. A social media service might be $50/month, while a CRM system will cost several thousand a month. I wanted to find out what this span looks like based on the type of technology being sold:

Middleware was showing much more expensive options for both their cheapest and most expensive tier, while the rest of the landscapes showed roughly similar rates.

One note on this data: there are far fewer middleware companies than companies in the other categories and as a result I’m hesitant to draw any particular conclusions from this outlier. It is entirely reasonable to hypothesize that the higher price of middleware is due to its being sold to larger organizations. While that may, in fact, be true, I don’t believe that we have enough data here to back that up.

How do marketing technology companies quote their pricing?

We found monthly pricing to be by far the dominant contract term:

This was roughly the same across all landscapes:

Clearly, the overwhelming majority of marketing technology vendors that list pricing publicly prefer to quote it in monthly terms. I would be extremely surprised if these numbers were the same for vendors who do not quote public pricing; my guess is that there are a far higher number of annual contracts quoted in that population. Still, if you’re a vendor and want to quote pricing publicly, the data is clear: most of your competitors are quoting in monthly terms. And they’re probably doing it for a reason.

There’s more marketing technology landscape data to come…

There are plenty more insights to be had from this data. If you’d like to read our next post analyzing the Marketing Landscape, subscribe to our blog.